The Santa Claus Rally was first recorded by Yale Hirsch, an analyst and author of the Stock Trader’s Almanac, in 1972. It is a calendar effect and was identified as a rise in stock prices in the last 5 trading days in December and the first couple in January. The ‘official’ Santa Rally does not start until late December. But, that does not stop headlines from being printed that attribute any market rise seen in the run-up to Christmas as the work of Santa. Much of this commentary, and indeed the initial work, concerns the US markets. However, unless the UK has been particularly naughty, perhaps Santa also gives FTSE 100 investors a present.

Has the FTSE 100 been naughty or nice?

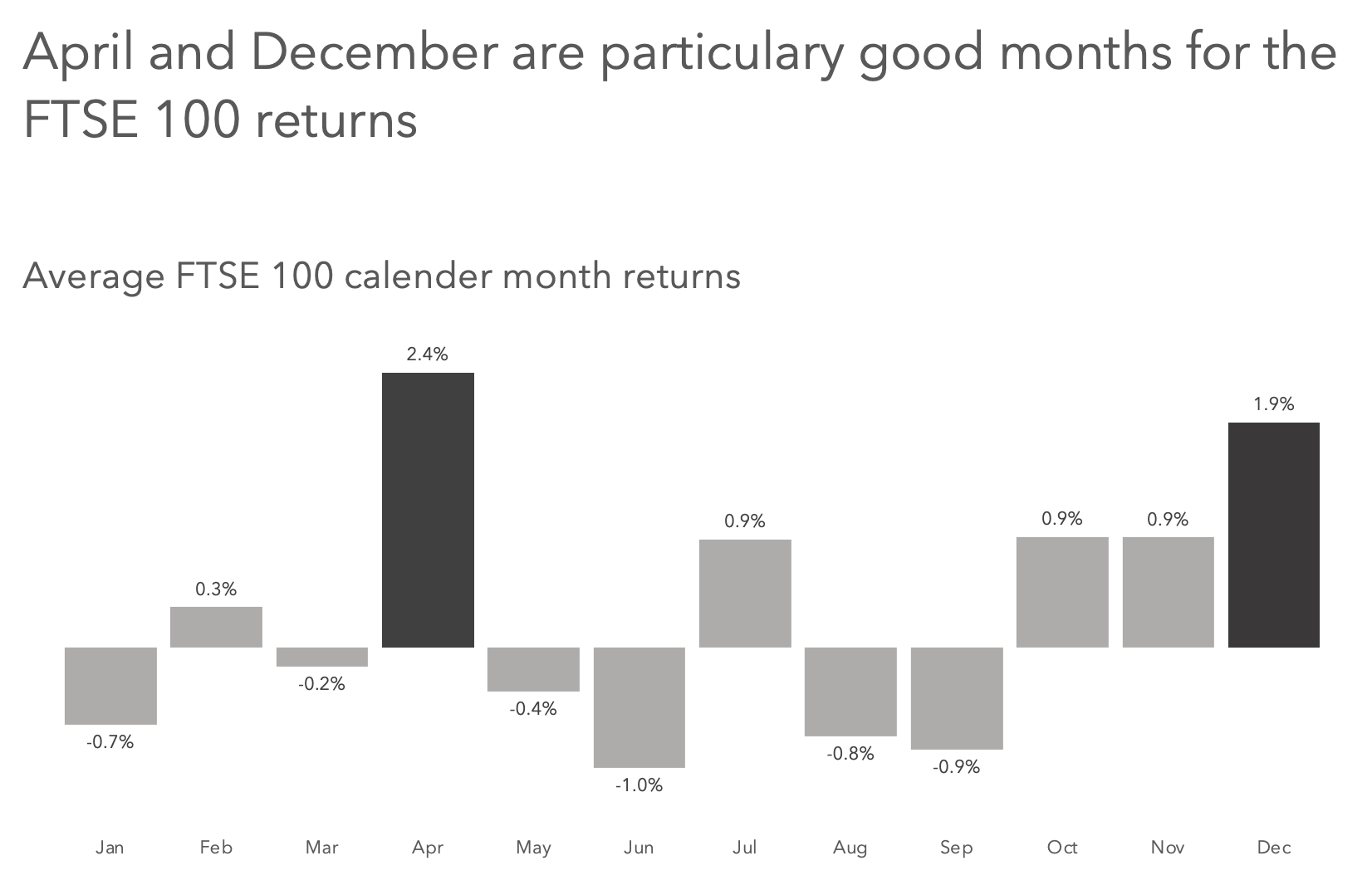

Using data from Yahoo Finance, I have calculated the calendar monthly returns on the FTSE 100 from January 1996 to November 2023. The returns are price returns, the change in the index number, these do not make dividend payments or reinvestment into account. A total return study, which does take dividends into account, will yield different results.

The mean average calendar month return is 0.3%. The standard deviation is a concerning 3.9%. The worst calendar month has been June, with an average return of (1.0%). December’s average return of 1.9% is the highest of any month except April’s 2.4%.

The standard deviation of December returns is the lowest of all the months at 3.0% (April’s is 3.2%. If we look at median rather than mean averages, December comes out on top with a median of 2.7%, followed by April on 2.5%. So, December has the second highest mean average return, the highest median, and the lowest volatility of return distribution about its mean.

If the index has been doing well until December, then December tends to be good

On the measures seen so far, December does appear to be a month where the FTSE 100 performs particularly strongly. However, if the FTSE 100 return from January to November is positive, then the subsequent December return also tends to be, and vice versa. A scatterplot of January to November FTSE 100 returns for each year since 1996 on the x-axis plotted against the December return for the same year demonstrates this relationship.

Running a regression with the January to November returns as the independent and December return as the dependant variable yields some interesting results. There is moderate correlation between the December return and the prior years return: the correlation coefficient is 0.43. Although the R square value indicates the Jan to Nov FTSE 100 performance explains only 18.5% of the variation in December returns, the overall model is significant (p-value for F statistic 0.02529), as are the coefficients (intercept p-value 0.00269, return prior Jan to November p-value 0.02529).

So, December does appear to be a particulary good for for the FTSE 100, but the prior years performance does have influence on just how good December tends to be. That’s what we would expect. A good year is usually capped off with a good month. Interestingly, December returns are not even weakly correlated with next years returns, implying there is a watershed moment at the end of the year.

Is there really a Santa Claus for large-cap UK stocks?

So, is the FTSE 100 Santa Rally fact or fiction? It’s more real than I would have guessed. There is evidence that December is a particularly good month (on average) for the FTSE 100, but the same appears true for April (perhaps the Easter Bunny also feels the need to boost the performance of large-cap UK stocks?). But then again, It does appear that if the year has been good for FTSE 100 returns then December tends to also be positive. So, the Santa Rally showing up does appear to be, at least in part, conditional on the index performance up to December.

It is always wise to be wary of historical patterns holding in the future. However, looking at the averages for the FTSE 100 calendar months, it may be thought that going long in February, April, July, and October through to December, and short at all other times would be a strategy that beats the index.

It is prudent also to be mindful that summary statistics like averages mask variability. The heatmap below does not attempt to hide the variability in the data. December and April do appear to pass the eye-test for being particularly positive months for the FTSE 100: there is a lot less red (negative returns) in their ledgers. The worst month on average, June does appear to have been a particularly troublesome month over the years. However, September holds the record for the widest range of outcomes, with two shockers (The FTSE lost 12% in October 2002, and 13% in September 2008) but also had a few high gain months: This wide range is easy to spot on the box plots further up the page.

FTSE 100 monthly returns from January 1996 to November 2023

The heatmap also serves to illustrate just what an extraordinary year 2020 was. The largest one month decline in the FTSE 100 since 1996 was recorded in March 2020. The largest monthly rise in the FTSE 100 since 1996 occurred in November 2020. The Great Financial Crisis, which kicked off in earnest in 2008 is also easy to spot.